Is GO+ by Touch ‘n Go a Good Place to Store Your Money? (Updated in 2026)

Summary

With so many investment options today, it can be hard to determine where to invest in Malaysia. Is GO+ by Touch ‘n Go still a good vehicle to park your cash? The short answer is yes, GO+ can be a decent place to park your short-to-medium-term cash.

This article breaks it down in terms of returns, safety, liquidity, then downsides to be aware of.

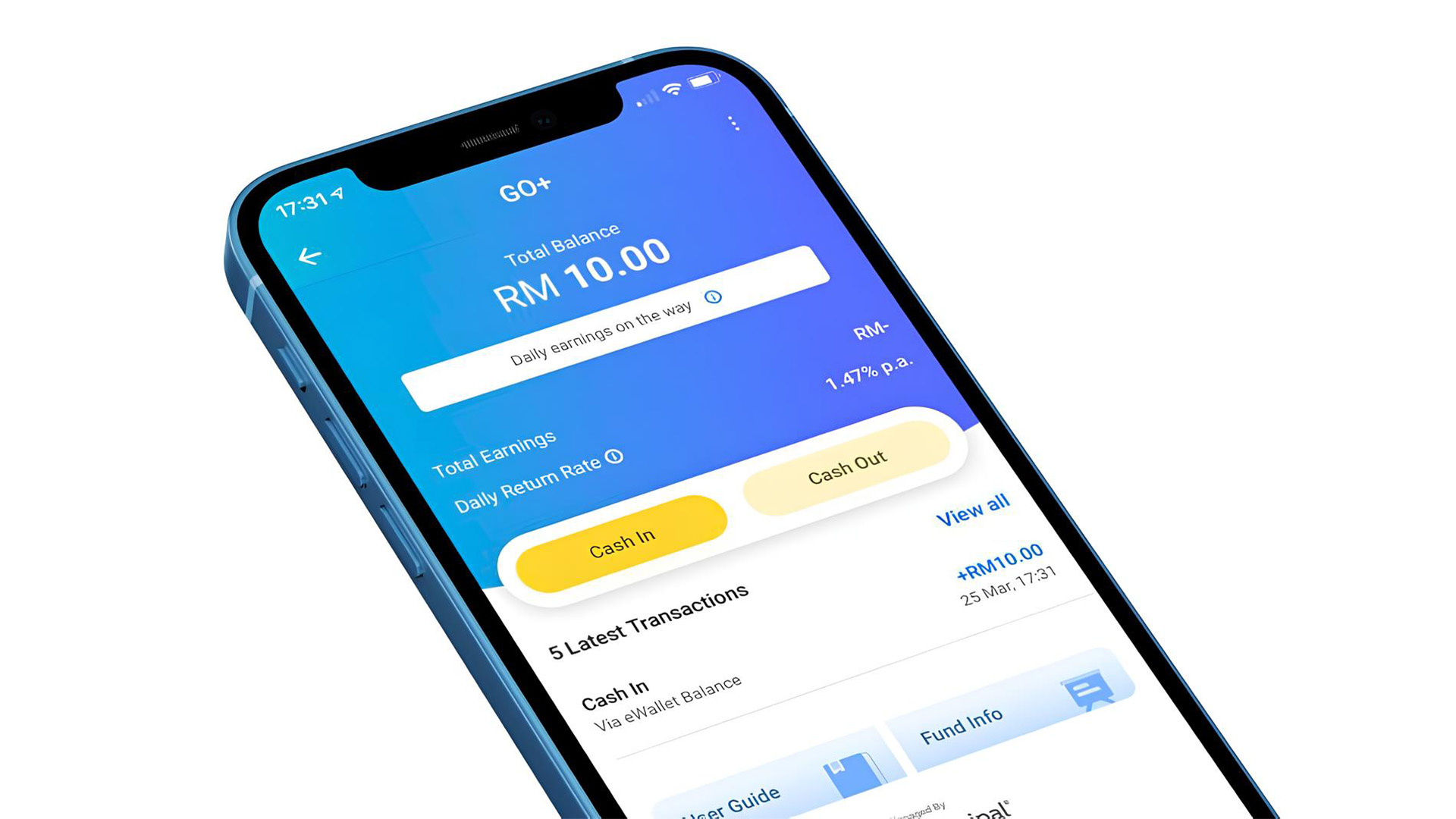

What exactly is GO+?

GO+ is a feature inside the Touch ‘n Go eWallet that lets you “store” money into an underlying fund called Principal e-Cash, which is a Shariah-compliant money market fund (a type of Unit Trust or Mutual Fund). It enables you to earn daily returns from as low as RM10. “Principal” is the fund house managing this fund.

Principal’s prospectus explains that the fund invests in Shariah-compliant instruments such as Islamic deposits, Islamic money market instruments, and sukuk, with specific restrictions designed for a liquid, lower-risk portfolio.

Returns: what you should expect from GO+

GO+ credits daily returns to your balance. The return rate varies from day to day, depending on the performance of the underlying money market fund. Historically, the Nett Daily Return Rate has been around 3% per annum, which is in a similar ballpark to Fixed Deposit rates offered by major banks in Malaysia. However, the returns vary on daily basis depending on the fund’s performance.

One upside that it has over fixed deposits is the liquidity it offers while enabling you to steadily grow your cash holdings. You are able to make withdrawals whenever you like, while keeping your interest accrued up until the withdrawal date. This is in contrast to some Fixed Deposits, where you have to hold until maturity.

Safety: the two types of “risk” people mix up

When people ask “Is Touch ‘N Go GO+ safe?”, they usually mean two things:

A) Investment risk (Principal e-Cash Fund)

As stated above, GO+ invests in a money market fund. These types of funds usually make their returns by lending out their liquidity (cash holdings) to large institutions for short periods of time. The advantage of this is they typically provide returns that are comparable to Fixed Deposits.

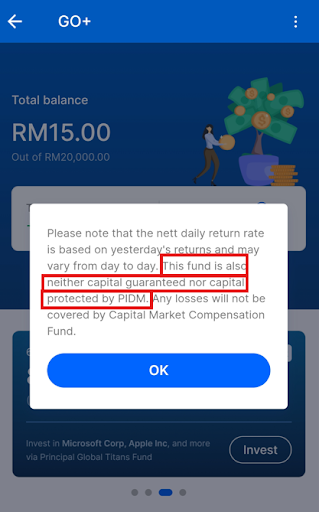

The main downside is that since GO+ is technically considered a type of investment fund instead of a bank deposit, it is not covered by Perbadanan Insurans Deposit Malaysia (PIDM). It is also worth noting that GO+ is not capital guaranteed and the underlying fund is not capital protected, which can be a turn-off for risk-averse individuals. However, the fund is managed by Principal, a well-established fund house, with a proven track record.

B) App and transaction security (your eWallet usage)

Separately, there is “account safety” in the practical sense: scams, unauthorised transactions, compromised access.

TNG’s Security Centre highlights steps and integrations they promote for user protection, including participation in Malaysia’s National Scam Response Centre (NSRC) and integration with Bank Negara Malaysia’s National Fraud Portal (NFP), plus an unauthorised transaction reporting flow with investigation timelines (subject to T&Cs).

Liquidity: why GO+ is popular for “parking cash”

One of the biggest plus points of GO+ is the liquidity it offers. It allows you to withdraw or spend the amount you have without worrying about losing accumulated interest, unlike Fixed Deposits where your accrued interest is forfeited if early withdrawals are made.

Moreover, GO+ is readily integrated with JomPay, which means you are able to pay bills directly from your balance if needed.

Touch ‘N Go has also made it easy to deposit money into the GO+ account, through the “Quick Cash In” concept where available balance above a threshold can be auto-transferred into GO+ (subject to conditions like non-transferable balances).

So, in liquidity terms, GO+ behaves like a convenient “cash parking” layer inside your eWallet, with the key difference being that it is an investment product.

Continue Reading: Capital Growth or Income Generation: Which is Better for You?

Identifying the Downsides of GO+

The downsides of GO+ can be broken down into 3 main aspects: no PIDM protection, low limits, and behavioural risk.

No PIDM Protection – The headline trade-off of GO+ is that it is not PIDM-protected because it is not considered a deposit.

Low Limits – Despite increasing its limit from RM9,500 to RM20,000 in 2024, it is still considered relatively low compared to other investment vehicles such as Unit Trusts or Fixed Deposits. This makes GO+ not ideal for individuals with a larger investment appetite.

Behavioural Risk – The high liquidity offered by GO+ means strong financial discipline is needed as being able to move money out easily can encourage overspending. This is especially detrimental if you are relying on GO+ to build an emergency fund.

Conclusion: so, is GO+ good for storing money in 2026?

Although GO+ is not the best investment in Malaysia, it is still a decent option for short-term cash that you want to keep liquid while still earning daily returns. However, if you are keen to find out where to invest in Malaysia for your financial goals, our personal financial specialists at Uno Advisers will be able to advise you on suitable investment options that suit your lifestyle needs.

Frequently Asked Questions

Q1. Is GO+ in Touch ‘n Go PIDM protected?

No. TNG states GO+ is an investment product and not a deposit, so it is not protected by PIDM.

Q2. What fund does GO+ invest in?

TNG states the underlying fund is Principal e-Cash, a Shariah-compliant money market fund managed by Principal.

Q3. What is the GO+ limit in 2026?

TNG’s Terms and Conditions state the GO+ account limit is RM20,000.

Q4. Can I cash out from GO+ anytime?

TNG’s help centre explains that you can cash out once your GO+ balance is at least RM10, and it provides in-app steps to cash out to your eWallet balance.

Q5. Are there fees to use GO+?

TNG’s help centre states zero sales (up-front) charge, with fund-level fees including management fee up to 0.45% p.a. and trustee fee up to 0.03% p.a., with returns shown after deductions.